| ✓ Pro | ⨯ Contra |

| Quick and uncomplicated | Risk of debt |

| Accepted almost everywhere | Card and foreign exchange fees |

| ✓ Pro | ⨯ Contra |

| Secure payment | Risk of forgetting to pay the invoice if you lose overview |

| Payment of invoice only after receipt of the goods | Some online shops only accept prepayment |

| ✓ Pro | ⨯ Contra |

| Quick and uncomplicated | Relatively high fees |

| Accepted almost everywhere | Need to keep depositing money |

| Expenses management, since only amounts paid in (pre-paid) can be spent |

| ✓ Pro | ⨯ Contra |

| Increased security because data is not passed on | Fees, especially for currency conversion |

| Partial buyer protection (as defined in GTC) | Complete security cannot be guaranteed (watch out for phishing mails) |

![]()

| ✓ Pro | ⨯ Contra |

| Works with almost all iOS and Android smartphones | Only works for Swiss online shops |

| Quick and uncomplicated |

| ✓ Pro | ⨯ Contra |

| Lower fees than for credit cards | Lower acceptance than for credit cards, e.g. for car rentals or hotel reservations |

| Quick and uncomplicated | Payments are debited immediately from the account |

![]()

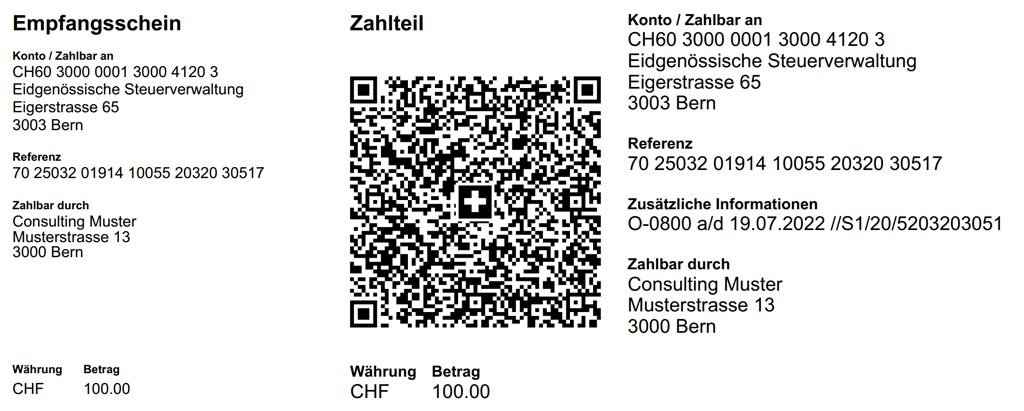

Note: Payment conditions vary depending on provider (such as Cembra Pay, Klarna, Powerpay, Twint, etc.).

| ✓ Pro | ⨯ Contra |

| Flexibility for larger payments | Risk of debt (reminder fees from the first reminder and interest on arrears) |

| No direct liquidity outflow | Possible credit score update |

| Only usable online; retailer acceptance varies | |

| Burden of payment obligations |