Market and price formation

Compare markets for everyday goods (e.g. bread or sunglasses) with the market simulated in Pitgame.

How are these markets different? In reflecting on these differences, pay attention to efficiency, competition and transparency.

What mechanisms are the same or similar in both markets?

The various buyers have different maximum purchase prices (reservation prices) for the same good. Conversely, sellers offer the same good at different minimum sale prices (reservation prices). Find possible explanations for these differences in the following examples.

Suppose you want to purchase a new laptop. Which factors influence your reservation price for the laptop?

Imagine you are a laptop manufacturer. What factors influence the minimum amount you charge for a laptop?

Consider the following starting scenario for a mini-pitgame/market:

| Buyers | Maximum purchase prices |

|---|---|

| A | 8 |

| B | 6 |

| C | 3 |

| Sellers | Minimum sale prices |

|---|---|

| D | 1 |

| E | 4 |

| F | 6 |

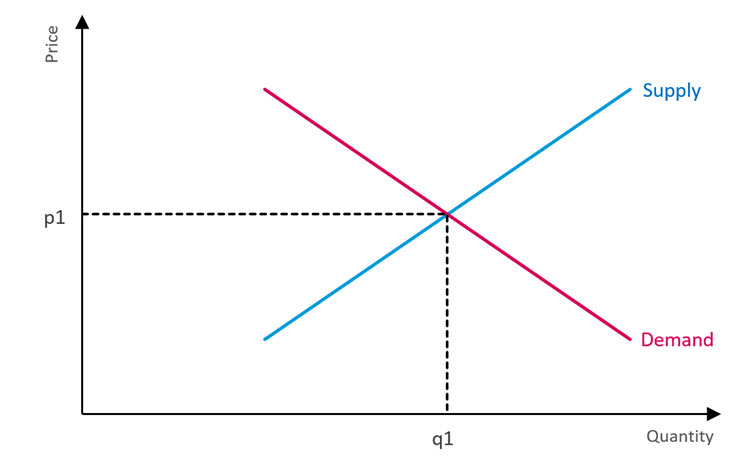

Construct the supply/demand curves. The number on the x-axis denotes the number of people who are willing to buy or sell the good. Bear in mind: the lower the price, the larger the number of people who want to buy and the smaller the number of people who want to sell.

How high is the equilibrium price?

Who can trade at equilibrium?

How high is the trading profit for all market participants?

What happens in the market when the price is 2?

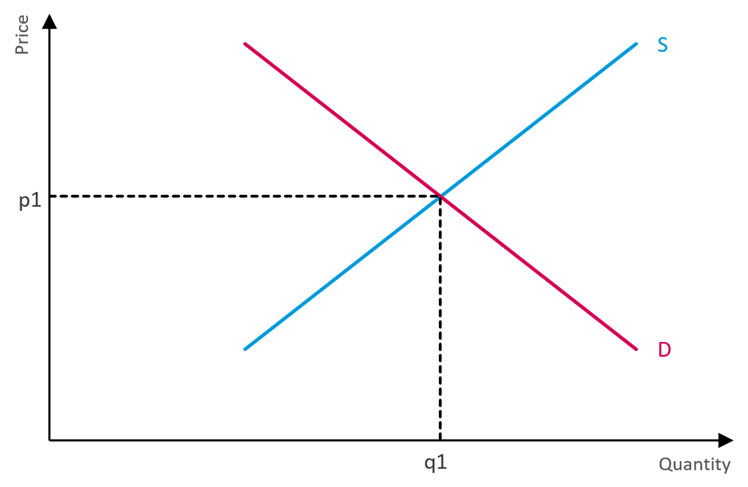

New hygiene regulations have recently been introduced for the manufacturing of a particular good that is traded on a commodities exchange. These new regulations slow down production.

How will this fact influence the starting scenario in Pitgame?

How does this new situation affect the equilibrium price for the good and the quantity sold?

Depict the new scenario graphically. Indicate how the curves shift and where the new market equilibrium lies. p stands for price and q for quantity. Thus, p1 is the initial price and q1 the initial quantity.

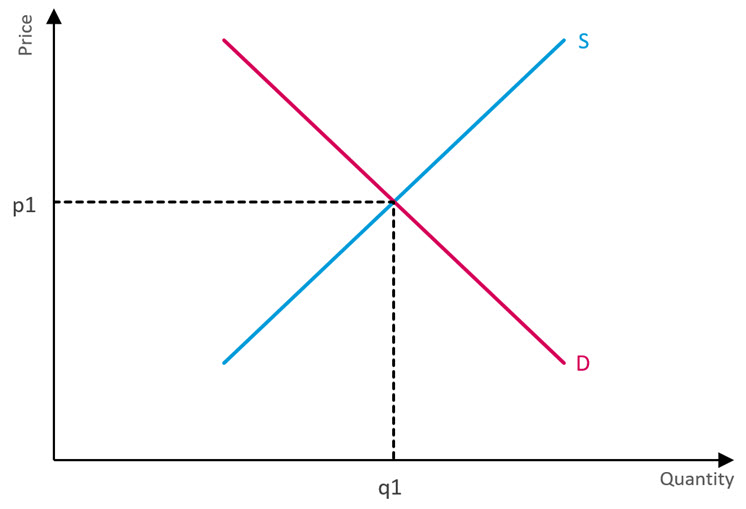

How do the following market changes affect the market equilibrium? Briefly explain your answers in each case and indicate how the curves would shift.

The commodity is less popular with customers as they can replace it with a cheaper one.

Technological progress enables a more efficient manufacturing process.

Let’s assume that the government deems the equilibrium price in Pitgame to be too high. It therefore sets a binding price cap, which is $3 below the equilibrium price.

How does this price cap affect the trades transacted in Pitgame? Study the following table listing the trades from the last round. The equilibrium market price is $38.

| Trade price so far ($) |

New price ($) |

Trading profit so far ($) |

New trading profit ($) |

|

|---|---|---|---|---|

| August/Franca | ||||

| Daniel/Dominica | ||||

| Beata/Mia | ||||

| Wolf/Gerry | ||||

| Roxanne/Gudrun | ||||

| Jens/Detlef | ||||

| Total |

How does the overall trading profit change?

Draw a conclusion: will the market participants profit from this government intervention? Explain your answer

In a well-organised, transparent and competitive market, the price will settle at a certain level. Who determines this price? Check the appropriate box and briefly explain your answers.

Which statements are correct? Check the appropriate box and briefly explain your answers